Recasting a mortgage vs refinancing

When you should recast a mortgage and when you should refinance

Mortgage recasting lets you pay down your mortgage and secure a lower monthly payment. You keep your original term, your original loan and the interest rate that you started with, but you have a lower principal value (because you paid it down), and therefore you have a lower monthly payment. Pretty simple, right?

Where it can get complex is when you start comparing recasting vs refinancing.

A visual breakdown: when you want to refinance and when you want to recast

Although there are no firm rules here (at the end of the day, it’s your mortgage and your choice), there are some general trends that we can easily apply to compare the attractiveness of recasting and refinancing.

The bottom line is that refinancing gives you a lot more flexibility. You can change your term. You can change you payment. You can change the equity you have in the home. You can refinance without any extra cash.

But, recasting also gives you the ability to do something refinancing can’t do, which is keep things the same. So, when you have a nice low interest rate, you can keep it!

Now, let’s make it personal. Type your info into the calculators to compare!

The only way to know which option is best for you is by using the real numbers for your real life situation. Below you will find two calculators with similar construction that can allow you to see what refinancing looks like for you, and what recasting would look like for you.

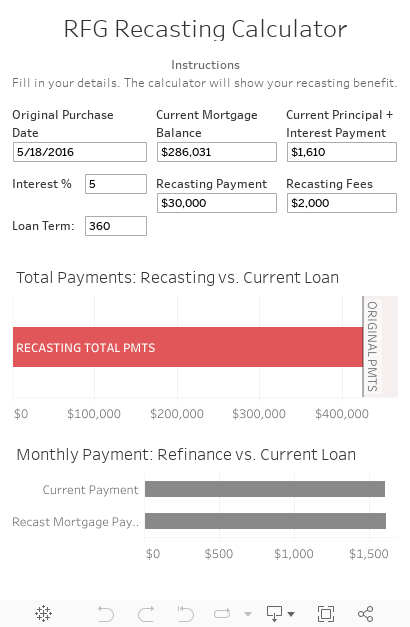

First, see what a mortgage recast would look like

The first step in comparing a recast to a refinance is looking at the numbers for a recast. In this case, the biggest lever (the principal payment) is set by you and it determines what the savings on the recast will look like for you. This calculator will show you the change in monthly payment as well as the total payments made during a recast as compared to the original loan.

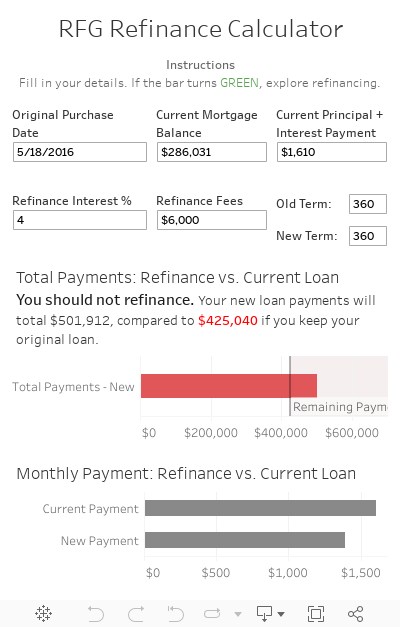

Second, look at what a refinance could do for you

With a refinance, there are a lot more moving pieces. The interest rate, term, and principal are all things that you can choose to change (although you will be limited to what a lender will offer to you, of course). If you need to see what a lender would offer to you, you can use Lending Tree to compare multiple lenders at once. That way, you can find the best offer for your situation and enter the details below.

Which scenario works better for you? It will depend.

With the calculators above, you should have a decent idea of what the two scenarios would look like for you. There is no rule for when someone should recast, and when they should refinance, but the most important thing is knowing that both of those tools are in your toolbox. They are options that you can take advantage of when it’s time to change your mortgage.

If you want to learn more about mortgage recasting, my original post on the subject goes into more detail about how you can obtain a recast from your lender, and which lenders offer recasts.