A calculator for when to refinance a mortgage

The refinance mortgage calculator

Knowing when to refinance can be tricky, and a little nerve wracking. It doesn't help that the financial media and blogosphere has made refinancing into ever more complicated calculations, all with their own terminology.

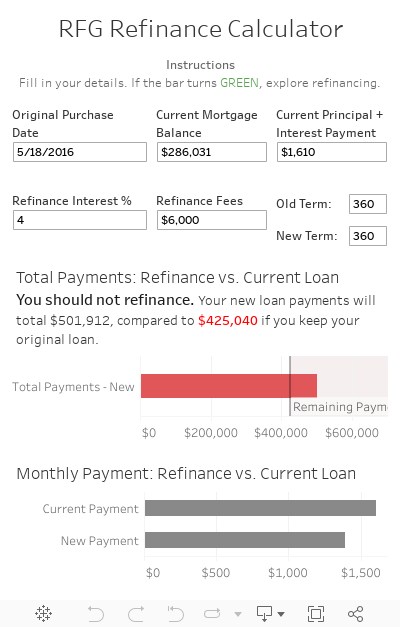

The calculator you see below is my attempt to simplify all of that. It asks a very simple question: if I refinance, will I end up paying less after I finish paying off my house?

Take a look. Enter the pertinent details of your current mortgage and potential future mortgage (don't forget fees...), and the calculator will automatically tell you whether it makes sense to refinance. Note that the calculator assumes a fixed interest rate, but you can adjust for any term of mortgage - the default is 30 years (360 months).

How to save the most when refinancing

People refinance for many reasons, but no matter what the impetus is the goal is always to save as much money as possible. As you can see from the calculator above, there really aren't that many levers to pull, so the goal is always to minimize the interest rate and initial balance. Here are some ways that you can achieve the lowest possible interest rate and initial balance for your refinance.

1. Lock in lower rates for your refinance with a 15 year vs. a 30 year

The easiest way to decrease the interest rate is to change the term of the loan from a 30 year to a 15 year mortgage (180 vs 360 months). In most cases, this will also bring a significantly lower interest rate. Interest rates are lower for shorter terms because the bank exposes itself to significantly less interest rate risk (the possibility that rates will rise and the loan will become comparatively less desirable as an asset).

2. Decrease your loan balance with equity financing

There are more ways to finance your home purchase than you might think. It may seem obvious, but the best way to minimize your payments is to borrow less money. With Point, you can sell a small stake in your home (10%-20%) in exchange for a cash payment now. Later on, when you sell or when you have the money to do it, you buy the equity back from Point at an appreciated price. I'd advise everyone that is refinancing at least explore this option before pulling the trigger on a new loan.

Note: Read the full post I wrote on equity financing.

3. Get a lower refinance rate by improving your credit before applying

It may seem patently obvious, but people with better credit get the best rates. If your credit score isn't well north of 700, then you will likely be able to get a better rate by improving your credit score. There are a number of ways to do that, but generally you want to develop a long history of on-time payments, decrease credit card utilization, and have 10+ accounts in good standing (whether closed or open). One way to improve two of those metrics at once is to consolidate high interest credit card loans, and maybe even student debt, into a single loan.

Conclusion

With rising rates, it's becoming more uncommon for people to refinance, but those with adjustable rate mortgages and higher interest short term mortgages will likely see some benefit even with the slow rise in interest rates.