Mortgage recast calculator: Figure out when to recast

What is mortgage recasting?

Mortgage recasting is a little known but useful trick that allows you to pay down your mortgage balance and secure a lower monthly payment while keeping your original loan and rate.

The basic principle is quite simple. You keep your original loan, your original term, and your original interest rate. The only thing that changes is the principal of the loan: you pay off a portion of the loan and the amortization schedule is adjusted to give you a lower monthly payment. Your payment is lower because you paid off a portion of the principal, but the term and interest rate are the same. This also lowers your total interest payments.

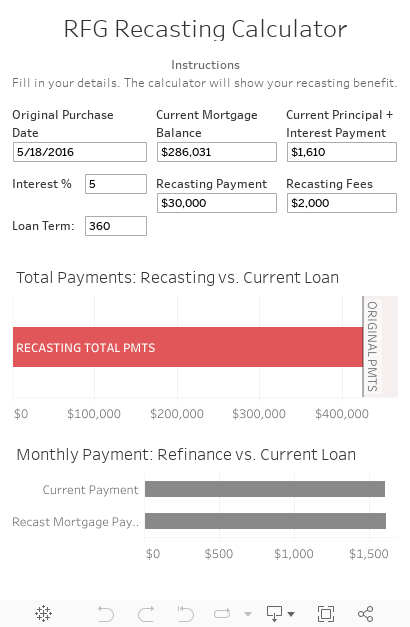

Use the mortgage recast calculator to see when to recast a mortgage

Knowing when to recast a mortgage is a personal decision. It isn’t quite as clear cut as refinancing, because the choice you need to make is if the additional principal that you are paying toward the mortgage could be invested more productively elsewhere. But, there are some very good reasons why someone might want to recast a mortgage which I will get to down below. For now, type in your mortgage details below to see what a recast could look like with your mortgage.

When should someone recast a mortgage?

There are a number of times when recasting a mortgage makes a lot of sense, but no matter what the homeowner will need to have a sizable chunk of change set aside to pay down the principal. Recasting is a process, and it’s really not worth going through unless the payment after the paydown will change in a significant way. I would say that you want to pay down at least 25% of your mortgage if you are going to recast, although that isn’t a “rule” so much as a guidepost to make sure you are using your time wisely.

Here are some situations when recasting makes the most sense.

Rates have risen - If your original mortgage is at 3% but rates are 6%, recasting is a smarter move than refinancing because you get to keep your old rate but secure a lower payment

You have a lot of money sitting on the sidelines - If you have a big chunk of change that you aren’t investing and that’s yielding less than your mortgage interest rate, recasting is a really good way to put the money to use and increase your month to month cash flow (from your lower monthly payment)

You need to decrease your payment to cash flow a rental - If you have a rental property with a mortgage that doesn’t currently cash flow positive, recasting a mortgage can help turn the tides. Of course, that doesn’t mean recasting is the best way to use that money (it could be that the rental just wasn’t a great investment…), but it is one way to solve that problem.

You are about to retire and you want to lock in a lower payment - Recasting can make a LOT of sense for people who are about to retire. Naturally, it’s preferable to have lower monthly bills as a retiree on a fixed income, and housing is usually a big line item. Recasting is particularly attractive in this scenario because the returns are guaranteed: you MIGHT make 7% in the stock market, but with recasting you immediately lock in a return equal to your mortgage interest rate… and that value can’t go up or down.

No matter what, the math for recasting is pretty simple. If you are going to make more money paying down your principal than you would putting the money someplace else, then it’s probably a good idea. It can even make sense if that isn’t the case, and you just want to secure a lower payment.

What are the disadvantages to mortgage recasting?

Although there are plenty of scenarios where recasting makes sense, there are some clear disadvantages as well. First of all, you are putting a lot of cash into the equity of your home, which is probably a good investment but it isn’t guaranteed, either. Second, it doesn’t change your interest rate so if rates have dropped it may not make sense. Third, it doesn’t change the term of your mortgage. And, finally, it costs money since the lender charges a fee for you to do it.

Who can recast a mortgage? Which banks offer recasting?

Although recasting is not universally available, it is fairly common with the main mortgage lenders. Those with FHA and VA loans will not have the option to recast, however. I’ve linked to the most helpful articles I could find for the three main lenders before, but you will probably have to do your own research as the banks don’t make it easy to find.

Your lender may also offer recasting but I cannot list them all here…

Conclusion: Recasting is a great tool, but remember all of your options

Although recasting is a very interesting tool, it isn’t your only option to apply excess funds towards a change in your mortgage. You can always pay down your principal with an extra principal payment, which has the affect of shortening your mortgage term. You can also refinance your mortgage (I go into detail on when you should recast and when you should refinance here). And, you can always sit tight and invest your money elsewhere!

Next week, I am going to take an in depth look at when someone should recast a mortgage, and when they should refinance.