Best time to buy a house

Why are homes a good investment, and when is the best time to buy a house?

A home is often the most expensive and most emotionally meaningful investment anyone will ever make. Even in affordable locations, houses are often hundreds of thousands of dollars, and in my hometown of San Francisco they can run well over $1m for very modest, smaller homes.

No matter where you live, buying a house is going to be financially significant, and to add to the stress, it’s also the place you are going to live, make memories, and potentially raise your kids. That’s what makes it an emotional investment.

All of this means that it’s PRETTY IMPORTANT to know when the best time is to buy a house.

Why houses are a good investment

In order to understand when the best time is to invest in a house, it’s important to fully understand the reasons why homes are a good investment in the first place.

A lot of finance bloggers say that houses aren’t investments, since you end up paying so much money in taxes and maintenance. Their argument is that it’s really more like a financial burden than an investment. Although I see their point, after my experience buying, renovating, and renting out my condo in Seattle, I can say that homes can be incredibly good investments. On a $150k investment (total), I’ve made well over $100k (on paper) in less than 4 years. It has taken a little bit of work, but it’s hard to argue with a 66% gain in less than 4 years.

So what are the underlying forces that are making this such a good investment?

Housing prices have a tendency to go up, especially over the long run

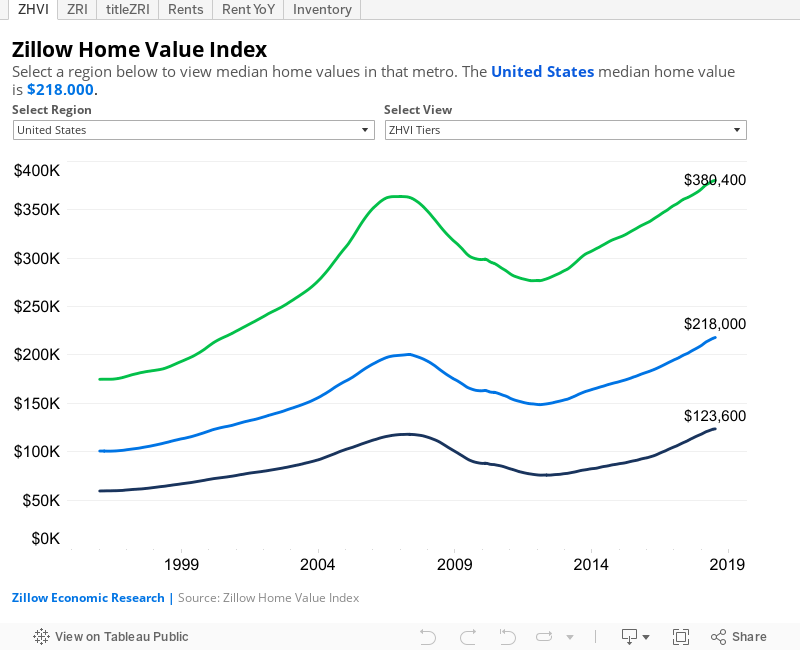

The economic expansion of the 2010s has been very good for the housing market, and prices have increased across the board. Below you can see a chart showing the average price from 1999 to present day. Despite the BIG dip in 2008, things have been firmly trending up. If you were to extend the timeline back, you would see a similar trend of price increases over time, with dips here and there. That’s why my grandparents are so flabbergasted that “houses in their neighborhood are going for $350k”… because they bought their house for $50k 30 years ago. The slow grind of appreciation can turn into big numbers over a long time.

Admittedly, prices can go down -and violently so as we saw in 2008- but over 20 or 40 year time span, prices have always gone up or remained level. Since the local market has been so strong in Seattle, my condo has appreciated around 30-40% in the past 3 years.

Those of you that are paying close attention might be raising your eyebrows because I said that I had made 66% on paper… how could I have made 66% if my condo has only appreciated by 30-40%.

One word: leverage.

Residential real estate gives you access to incredible leverage

I never would have been able to purchase my condo without a mortgage, and then I would have never been able to take part in the rising prices in my neighborhood over that time. The 30 year mortgage allows nearly anyone in America to participate in the housing market because it spreads out the cost of the home over a very very long time. It doesn’t hurt that the interest on the mortgage is tax deductible, either!

In addition to making homes more affordable, a mortgage magnifies returns. If you spend $1 and borrow $9 to buy something worth $10, and its price goes up by 20% to $12, you just 3x’d your money. This is because you could now sell what you bought for $12, leaving you $3 after paying off the loan, and 3 is 3x1. Quite simply, there is no other opportunity for leverage like this for us “ordinary” people.

Leverage is the reason why the 30% gain on my condo is actually 66%.

When will I know it’s a good time to buy a house?

The best time to buy a house is when you can maximize the positive attributes of owning a home. In other words, you want to be able to see the most appreciation, and the most beneficial leverage. Here are some key indicators that it COULD be a good time to buy a house. Keep in mind, I am not telling you to buy a house, and every situation is different. But… if you find a house under these conditions there’s a good chance it is a better investment than if it doesn’t meet these parameters.

You can buy now and hold the house for the long term

Housing investments pay off OVER TIME. It takes time to pay off the mortgage. It takes time for appreciation to run its course. That is why the most important correlating factor to whether or not it is a good time to buy a house is whether or not you can stay there or own it for at least 10-15 years. Houses are expensive to buy and sell because of broker commissions, fees and taxes, so you really don’t want to be moving a bunch. Also, mortgages are designed so that you pay your interest up front (look up an amortization table). All of this means that the longer you hold your home, the better you will do.

The house is cheaper than it was recently

Since housing prices go up over time, it can be difficult to “time the market”. In periods of economic expansion, it can feel like prices are always rising and that you will never “get a good deal.” This was true for me when I bought my condo in 2015. Prices had been going up for 4 years and I thought I MUST be buying in at the top of the market. As it turned out that wasn’t the case at all, but it could have been.

The point of all this? If you happen to be searching for a house and prices have feel significantly from their peak, it could be a good time to buy. For instance, in 2011 and 2012. The housing market was depressed and languishing at that time after the steep drops from the peak in 2008, and it was a great time to buy in hindsight.

One thing about this: some markets are cheap for a reason! If the house you are looking at is going to be (literally) underwater in 5 years, or they are putting in a coal powerplant next door, there’s a good reason why the place is cheaper than it was and it is likely to remain that way.

You can get a good rate on a long term mortgage

Again, if you are doing things right you are already planning to own the house for a long time. This means that you can line up an affordable 30 year mortgage. It’s important to shop around for the lowest rate possible with companies like Lending Tree that can cross-compare multiple lenders at the same time, giving you the best possible rate.

Historically, rates below 4% are crazy good, rates below 5% are good, and rates 6% and below are manageable. If you have to pay above 6% you are going to be paying a ton in interest and it may not be a great time.

So… the best time to buy a house is…

In summary, the best time to buy a house is when prices have gone down, mortgage rates are low, and you are prepared to stay in the home for a long long time. Under those circumstances, historically, it’s hard to make a bad housing investment unless you are buying in a bad location.