PMI removal calculator: How to get rid of PMI

Calculate your equity to get rid of PMI

I'll be right up front with it. PMI (Private Mortgage Insurance) is the biggest ripoff in real estate... but not necessarily for the reason you'd think. PMI itself makes sense. If you can't pay for a standard 20% down payment, your bank will make you pay for PMI to insure their loan against default. So, PMI is a reasonable concept overall, but it's still a huge ripoff.

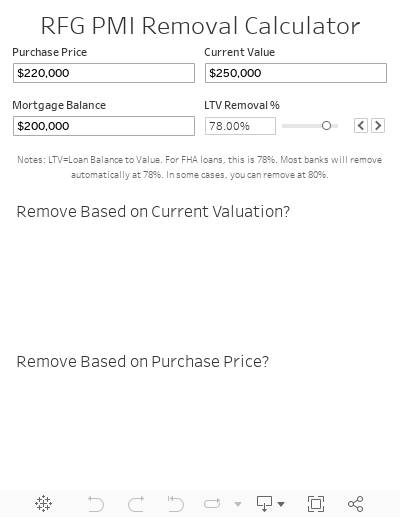

After the price appreciation since 2012, millions of homeowners have more than 20% equity in their home and could have their PMI removed or refinance into a new loan without PMI. But... they're still paying it. Use this PMI removal calculator to see if you can remove yours.

If one of the bars turns green and says "Yes", you should be able to remove your PMI. If they are both red, you'll see how much more equity you have to build before it can be removed. Here it is, the remove PMI calculator, or more accurately, the "When can I get rid of PMI calculator".

Hopefully, you can remove your private mortgage insurance PMI? Or, refinance into a loan without PMI? Or, at least you have some better context for when does PMI go away? Or, when PMI will be eliminated based on the current value of your home. I'll let you know how to actually go about removing your mortgage insurance premiums below, but I wanted to add a little context from my mortgage insurance experience first.

PMI: A Necessary Evil

Like many these days, I bought a home in an expensive coastal city, with expensive coastal listings and I only put 10% down instead of the standard 20%. I did this intentionally so I'd be able to more easily afford remodeling the condo I bought.

Unfortunately, since that meant I had less than 20% equity in the home, I had to settle for PMI as well. This ended up costing $120 a month; it didn't break the bank but it wasn't pleasant, either. I certainly wasn't the first with PMI, either. It's a necessary evil in cities like Seattle, San Francisco and New York with expensive housing and competitive markets. I wish I had known the techniques for avoiding PMI that I know now, but you live and learn. One thing is for certain: from the moment I started paying PMI I was wondering how to get rid of PMI insurance.

How to get rid of PMI: My favorite methods

After my first PMI payment, I knew I wanted to get rid of it as quickly as possible. It's actually not that hard to do, but the banks don't make it easy to do quickly. Here's what I mean:

When does PMI go away? Most banks will automatically remove PMI when the loan balance has reached 78-80% of the value of the original purchase price. In other words, if someone buys a house for $100,000 and puts $10,000 down (giving you a $90,000 mortgage), once the mortgage is paid down to $80,000 the bank will automatically remove PMI. For FHA loans, that number is usually 78%, and every bank is different.

You can also get starting removing PMI by proving to your bank that your home has appreciated enough to bring your LTV (Loan to Value) ratio down to 80%. In the same example as above, if your $100,000 house appreciates to $120,000 then your $90,000 mortgage is less than 80% of the home value. BUT... you have to get an appraisal to prove your homes appreciation.

Maybe this is obvious, but you can also refinance if you have built up enough equity so that your refinance loan will be over a 20% LTV. I wouldn't necessarily recommend this unless you also want to take cash out for other investments, or you can get a lower interest rate. If you do refinance, LendingTree is a good place to check for rates.

It can take 4-6 years for PMI to be automatically removed through option (1) above, or longer if the down payment was lower than 10%. Since home values have gone up so much recently, there are probably millions of people who have enough equity to remove their PMI via option (2), but may not know that they can.

How I knew I could start getting rid of PMI

In my case, I knew I would have to get an appraisal. The moment i remodeled my condo (thereby adding value to the home), I started the PMI removal process by contacting Wells Fargo directly. They pointed me to an approved appraiser who valued the home at juuust over the number I needed to meet the 80% LTV value and have my PMI removed. (Note: I talk a little bit more about that, and my experience as a rental condo landlord in this post).

The total cost was around $600, which equates to about a year of PMI payments. But, it would have been 4-5 more years before PMI was removed automatically, so I saved thousands overall.

If you didn't type in your numbers into the calculator above, give it a go. Don’t know your numbers? No problem.

You can track your homes value (and the rest of your finances) for free with Personal Capital. Simply sign up for an account, enter your home as a new asset, and then you will see its Zillow Z-estimate displayed as below. Enter your mortgage as a separate account for the full picture. Then, enter the values you see on your Personal Capital dashboard into the Current Value field in the calculator above.

Use Personal Capital to keep track of your home equity, along with the rest of your investments

So, can you remove your PMI?