How to avoid PMI without 20% down

How can I avoid PMI without 20% down?

Private Mortgage Insurance, or PMI, is an annoyance that nearly every homeowner has had to deal with at some point. The simple fact is that most first time homebuyers don't have the ability to put down the 20% or more that banks require, so PMI is slapped onto their monthly payment to ensure that the bank gets paid - even if the homeowner defaults. It’s insurance, simple as that.

It doesn't help that real estate is appreciating at a rapid pace across the country, making it even harder to meet the 20% downpayment threshold. When I bought my condo in Seattle, I only had 10% to put down on the $321,000 purchase price - and I had to scrape that down payment together as it was. If I was buying now I would have had to put even less down because prices have gone up another 25%.

If you’re looking for a home now, you’ve probably already resigned yourself to the conclusion that you are going to have to deal with PMI. But…

“Guess what? You don’t need 20% down to avoid PMI.”

Today, I am going to go into detail on three amazing techniques you can use to avoid PMI without 20% down.

Use an equity partner

Get a primary mortgage and an alternative loan

Use a lender that doesn’t require it! (BONUS: List of lenders that don’t require PMI included!)

#1: Use an equity partner

The world of finance is exceedingly complex, but there are really only two ways to raise money from other people: rent it from them by borrowing (so, a loan), or selling a part of your ownership. The vast majority of homeowners choose to borrow money from the bank in order to pay for their home. It's easy, and there is a huge network of banks and mortgage companies that make it easy.

But, there is also a way to sell a portion of your ownership in your home in exchange for equity. Or in the case or new homeowners, you can take on a partner like Unison (or it's competitor Point) who will give you a cash payment in exchange for equity in your home.

A real life example of using an equity partner

Let's say I am buying a $500k house. Ordinarily, I would need to come up with $100k for a downpayment, but I only have $50k. Unison will fork over the other $50k in exchange for a percentage ownership in the home (in this example, it’s 35%).

Because I am putting $100k down (Unison is providing $50k of it), the bank does not need to apply PMI. The best part is that there are no monthly payments for Point or Unison since they are purchasing a share of the ownership in the home.

It’s a good deal for them because they paid 10% for a 35% share in the appreciation of your house. It’s a good deal for you because you can buy more home with a smaller loan and no PMI.

Downsides to using Point or Unison for equity financing

Here’s the catch to all of this. When I sell, Unison will take 35% of the appreciation, but I get to hang on to the rest as normal. So, in our example of the $500k home, if the home goes up by 20% to $600k, then Unison gets to keep 35% of the $100k gain, or $35k. You can see how this works below:

If the home goes down by $100k in value and I sell, then with Unison the same thing happens in reverse: they shoulder $35k of losses so their stake is only $15k. With Point, the numbers are a little more punitive when the value goes down, in other words they keep more of their equity at the expense of yours.

Point does have one advantage in that you can use them even AFTER you have purchased your home, theoretically enabling you to remove your PMI if you have it. However, they will try to undervalue your home thereby giving them a greater stake in the appreciation. There’s always a catch.

If equity financing doesn’t make sense for you, there are definitely other methods to avoid PMI.

#2: Use a primary mortgage and an alternative loan

If you can afford the monthly payments that PMI would bring, but you don't want to throw the money down the drain, then a second mortgage or loan would help to get around it. The concept is fairly simple: if you can borrow enough money to ensure that your down payment is over 20%, then you won't have to worry about PMI.

This isn't necessarily a foolproof system. Lenders will look into total indebtedness and people who are already up to their eyeballs in debt are much less likely to get approved for their mortgage. However, those who have the income to cover the payments (and still survive), could easily use this method to avoid PMI.

Some mortgage brokers will help buyers set up two mortgages to achieve exactly this. In my mind, it would be much easier to get a personal loan through Lending Tree, provided that the amount needed wasn't too high. The other benefit to using a personal loan is that they are significantly easier to get, although the rates may be higher.

Downsides to using a primary mortgage and alternative loan

This method is pretty complex. You’ve got two loans, usually with two separate lenders meaning two applications and two payments. It also results in a higher monthly payment than using an equity partner, but you do own the whole house.

#3: Use a lender that doesn't require it!

The easiest way to avoid PMI is by using a lender that doesn't require it for down payments below 20%. In my native San Francisco, the San Francisco Federal Credit Union has a program they call "POPPYloan" which enables VERY high earning households to finance up to 100% of their home purchase, up to $2 million. The program is only available for 9 Bay Area counties, but for those of us in San Francisco it's certainly a viable option.

There are tons of other mortgage programs from traditional banks like Bank of America and Suntrust, along with the VA and FHA that can allow for very very low down payments as well. It’s not that hard to avoid PMI simply by choosing the right lender, and it may surprise you that many of these options are very friendly to people with lower credit scores (in the 600’s). Here’s my list of lenders that don't require PMI.

Home loans that don’t require PMI

Bank of American Affordable Loan Solution

No PMI

Biggest advantage: 3% down

Biggest disadvantage: Cannot be an existing homeowner

San Francisco Federal Credit Union POPPYloan

No PMI

Large loan balances possible

Biggest advantage: 0% down

Biggest disadvantage: High income needed

No PMI

Large loan balances possible

Biggest advantage: Can use future income potential to qualify

Biggest disadvantage: Credit score of 720+ needed

No PMI

Biggest advantage: 3% down

Biggest disadvantage: Not available in every market, have to hold one months mortgage payment in reserve

No borrower paid PMI

Biggest advantage: Rate discounts for existing customers

Biggest disadvantage: Minimum credit score of 680

Suntrust Agency Affordable Financing

Low PMI

Biggest advantage: Can use gifts or seller contributions for down payment, can roll closing costs into a higher rate

Biggest disadvantage: Still has PMI…

NACA (Neighborhood Association)

Low PMI

Biggest advantage: Low and alternative income friendly

Biggest disadvantage: Strict qualification criteria (you need to be in the right area to qualify)

Reduced PMI rates

Biggest advantage: Low credit threshold of 620

Biggest disadvantage: Still has PMI…

Reduced PMI rates

Biggest advantage: Can have any loan term (e.g. 22 years) at 3% down

Biggest disadvantage: Still has PMI…

This Forbes list is also an excellent resource for no and low down payment options without PMI in local areas.

My guess is that this type of mortgage will become more popular over time.

Downsides to a low down payment mortgage

Any 0% down mortgage has one huge disadvantage: the payments are going to be through the roof! Not only will interest rates be higher than with a standard 20% down mortgage, but you are financing 100% of the purchase so it is just naturally a bigger mortgage with bigger payments.

If it were me, and I wanted to know how to avoid PMI without 20 down, I would probably still prefer to use Unison as an equity partner than lock myself into a gigantic mortgage payment for years to come. I am sure there are people who would look at Unison as an enormous ripoff, though. Different strokes for different folks!

Conclusion: avoiding PMI without 20% down is not that hard!

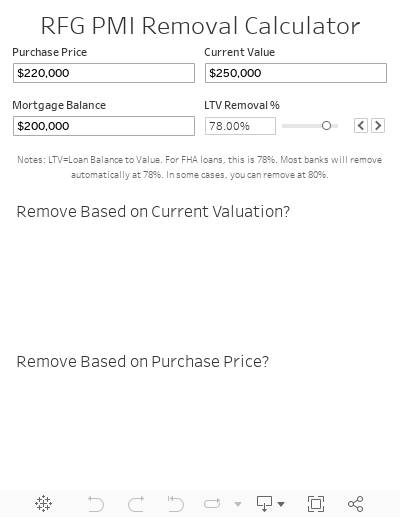

The bottom line is that you don't have to put up with PMI. If you are creative, there are lots of ways to avoid PMI without putting 20% down. There are also many ways to get rid of it, which I detailed in a dedicated post on the matter before. If you have PMI and you want to calculate if you've reached the threshold to remove it, simply scroll down!

Here's to no PMI!