What is an ISO? Incentive Stock Options Basics

Incentive Stock Option Basics: What is an ISO stock option?

tl;dr: ISOs (incentive stock options) vest over time, giving you the ability to purchase shares at a discounted rate and participate in the (potential) rise of your employers stock. If used properly, they are also tax advantaged.

For anyone working at a startup or technology company, a significant amount of compensation (and therefore a significant benefit) will likely be in Incentive Stock Options, also frequently referred to as “Stock Options” or “ISOs”. But, what is an ISO? ISOs can be difficult to understand in concept, and although there is a large amount of information that is publicly available, it’s often written in opaque and confusing language. For instance, the Wikipedia article on ISOs, which I recommend that you read after reading this. Sometimes, you just need the basics.

When I received my first option grant, I immediately started researching and trying to understand the best way to take advantage of my ISOs… and avoid the potentially bankrupting mistakes I had read about. This series will provide you an in depth look into the information I’ve gathered, along with resources to understand the value and potential of your own ISOs. Keep in mind, I am not a tax attorney or a financial advisor, so you should research this for yourself as well.

What are incentive stock options and where did they come from?

An Incentive Stock Option is the opportunity to purchase shares in a company you work for at a fixed price, sometime in the future. That’s it. You have the choice… the option… to purchase your employer's stock at a fixed price. Presumably, as the company acquires customers, raises revenue and achieves other goals, the value of the company will rise, and so will the value of the choice to purchase part of the company. ISOs are a tangible way to encourage employees to pursue the interests of their employer. They are also tax advantaged, something which I will go into more detail about later.

The modern history of the ISO began with Fairchild Semiconductor in 1957. A group of 8 scientists and researchers left their previous employer (Shockley Semiconductor) and started their own company, Fairchild Semiconductor. Lacking the resources and capital to finance the company themselves, they raised capital from Sherman Fairchild and in return for their efforts and expertise, were each granted a small stake in the company. Although this was significantly better than their situation at Shockley, where they had no ownership at all, it still amounted to a small slice of the company relative to their contributions. Perhaps more importantly, Fairchild (the parent company) was against offering any stock to other employees as an incentive, something the eight were particularly eager to do in an effort to retain talent in highly competitive Silicon Valley.

Seeking more enlightened pastures, two of the eight, Gordon Moore and Robert Noyce, left Fairchild to found Intel in 1968. In doing so, they ensured an enormous ownership stake for themselves (later worth billions), as well as an Incentive Stock Option plan for their employees: everyone that worked there would have a stake in the organization. From then on, nearly every technology company from Apple to Zynga has included ISOs as a core tenet of their compensation philosophy. There are some exceptions, like Netflix, but generally if you work in Silicon Valley you can expect to receive stock of some kind (although it won’t always be in ISOs… which we will discuss later).

What is an ISO stock option and how do they work?

There are a couple of terms that are important to discuss right away, which I’ll try to break down into easy to understand blocks. At their core, all ISO stock options have three components: quantity, price, and time. These components will vary from company to company, and within each grant. Typically, the language of an initial grant in an offer letter will look something like this:

Subject to the approval of the board, company XYZ grants [Your Name] 1200 shares of XYZ stock. ¼ of these shares will vest on 1/1/2018, with 1/48 to vest monthly thereafter.

You’ll notice that the price component is conspicuously missing there. Normally, price isn’t noted in offer letters because the value of privately held companies changes month-to-month, based on a determination of the board and their advisors. In English: you’ll know the price of your shares in a month or so, after the board fixes the price for that month. In Part II of the series, I will go over some methods of determining the value of shares in an offer letter, so you can understand what you are accepting before you do.

Let’s say for simplicity sake that the value for the grant in this example is $1.00 per share.

Breaking down the basic components of an ISO stock option exercise

Basics of an ISO Exercise #1: Quantity

This is by far the easiest of the components to understand. You are being granted a certain number of shares, in the example above it’s 1200.

Basics of an ISO Exercise #2: Price

In this example, the STRIKE PRICE, or the price that you will pay to purchase your shares, is $1.00. There is also the EXERCISE PRICE which is the value of the stock on the day that you purchase the shares. The difference between those two is the amount of money you will make, per share, if you sell the shares on that same day. For instance, if you exercise the stock when it’s value is $10 per share:

Exercise price: $10.00 per share - Strike price: $1.00 per share = $9 per share profit

Then, you can multiply the number of shares by $9 to arrive at the net gain. For instance, if you sold all 1200 shares in the example grant, it would be 1200 x $9 = $10,800. Subject to taxes, of course.

This also illustrates that you want the strike price to be as low as possible, in order to maximize the value you gain from the sale of your shares. For instance, if a different employee were to join the company two years later, and receive the same 1200 shares at a strike price of $5 per share, they would only make $5 per share ($10 exercise price - $5 strike price) instead of $9 per share. In this way, incentive stock options benefit early employees at startups, because they have to pay much less for their stock. In many cases, they also receive significantly more shares in their grants than later employees.

Basics of an ISO Exercise #3: Time

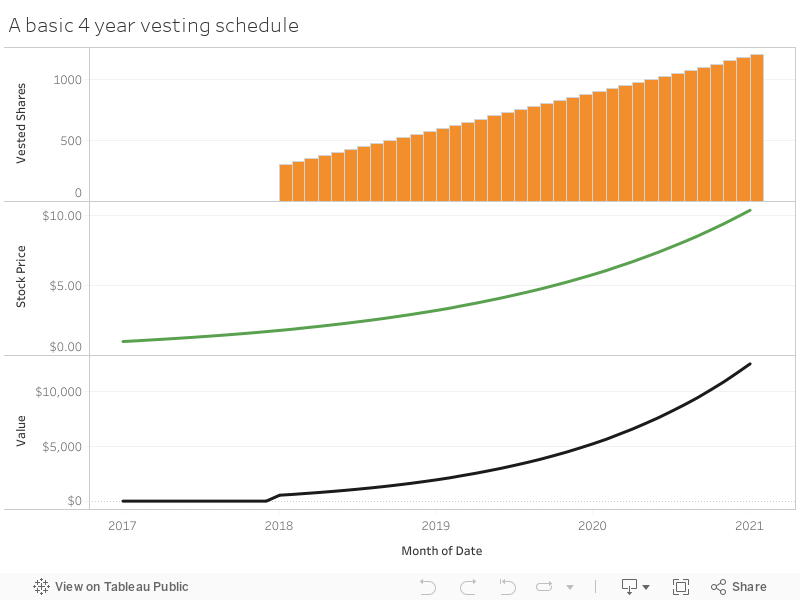

The example above is a very typical option grant. You will VEST, or be able to take ownership of, 300 shares (¼ or 25% of the total grant of 1200 shares) exactly one year from today. This is often called the VESTING CLIFF, because on a chart showing the vesting schedule, it appears like a giant cliff. After that, you will vest 1/48th of your total grant (25 shares) each month until you have vested the full amount of 1200, which will occur exactly 4 years from the date of your grant.

Sometimes it’s easier to see this stuff visually. Here's the same view from the top, but now you have some more context.

So, what does it all mean when you put it together?

First of all, your stock options are meant to be an incentive to work harder and stay longer, which is why they vest over time. The vesting cliff is there to ensure you put in a full year of service before you can see any financial benefit from your options. After the cliff, you get a little slice of shares each month going forward.

As the value of the company rises (price per share above), and the number of shares you have vested (the number of shares you are able to purchase) rises, so does the total value of your grant. I should note that in the example above, the stock price increased over 10x in the four years of the grant. Although that isn’t an unheard of number, it is a significant gain, and you should ground any expectation of the stock price of your company firmly in reality.

However, this does illustrate the power of ISOs as a wealth generator and incentive. If the company does well, so will you.

Exercising, selling, and monetizing your ISO employee stock option shares

In order to take advantage of your grant, you need to exercise and (eventually) sell your shares. You are able to exercise as many shares as you have vested at any given point. In the example above, you would be able to exercise 300 shares on 1/1/2018, 325 on 2/1/2018, 1075 on 8/1/2020, or the full 1200 on 1/1/2019. For a multitude of reasons that we will cover later, your choice on when to exercise your shares will be the most crucial decision in maximizing the amount of money you get from your grant… and minimizing the amount of tax you will pay on them.

After you exercise your employee stock options, you need to sell them to turn your ownership into money. In the past, if the company who issued the grant wasn’t publicly traded on a stock exchange like the NYSE or Nasdaq, it was almost impossible to sell shares from an ISO grant. This is why IPOs are glorified in technology circles: without one, no one can sell the shares that they own and realize their gains. Nowadays, and especially with the rise of the Unicorn companies (private tech companies who have not gone public), there are a host of private markets that make selling privately held stock easier. However, it’s still difficult and comes with it’s own set of challenges.

Assuming the company has gone public, then the process of exercising and selling your shares is actually extremely simple. There are two basic types of exercise:

Straight Exercise: You pay the strike price ($1.00 per share in the example above) from cash, and all of the shares you exercise are then deposited in a brokerage account.

Sell to cover: You pay the strike price for your entire exercise by exercising and selling a portion of the shares. For instance, if you want to exercise 1000 shares at $1 a share, as in the example above, and the stock price is currently $100, then 10 shares will be sold to cover the exercise cost ($1000=$100x10). After selling the shares needed to cover the exercise, 990 shares are deposited in your account.

With either option, and again assuming the stock is publicly traded, you can choose to sell or hold the stock you purchase.

Want to learn more about stock options?

If you work for a startup or technology company, chances are that equity (stock) is a big part of your compensation. But do you understand it? Do you know how it’s taxed? Do you know how to take advantage of your equity to the fullest? Read my book to arm yourself with the information you need.

The following posts will also be very helpful for you.

Conclusion

Incentive Stock options are a fantastic way to build wealth outside of traditional investment vehicles, and you should be happy to receive any grant big or small. However, there’s a great deal more to cover in the rest of the series, so make sure to read on.