How to value stock options in a startup

How to value stock options in a startup

One of the biggest challenges people face when evaluating job offers that include Incentive Stock Options is understanding the current -and potential future value- of their ISO stock option grant. In order to do that, you have to know how many shares you have, how many shares there are total, and a rough estimate for how much the shares are worth now. Let’s take a look at why, before we delve into how to find those numbers.

Why do we need so much information to value a stock option grant?

Grants can be difficult to value because companies usually only disclose the number of shares being granted, rather than the number of shares being granted AND the total number of shares, AND their current value per share.

Why should you care? Well, 1000 shares currently worth $1 a share are worth a total of $1000, but if they’re only worth $0.10 per share… then the grant is only worth $100. That's a big difference in value with the same 1000 share grant.

Oddly, the grant with the lower value per share might end up being more desirable, because the value per share on the day of the grant becomes the strike price. As we went over in Part I, the strike price is the price you pay for the shares. Because of that, you want the share price to be as low as possible when you get your grant, and as high as possible when you end up selling your shares. When people join later stage startups with higher valuations and (generally) higher grant dollar values, it becomes even more important to know the value per share so you know your cost to purchase. It doesn’t matter if your stock is worth $1,000,000 if you have to pay $999,999 to buy it.

Knowing the present value of your grant is an important piece in finding the value of your grant, but so is the potential future value. To find the future value, you have to have a ballpark figure for the percentage of the company that you have been granted. If you know how much of the company you own, you can guestimate the valuation of the company at IPO or acquisition, then simply multiply by your ownership percentage to get a future valuation for your shares.

For instance, if you are being granted 1000 shares, and there are 100,000 shares total, you’ve been given 1% of the company. Conversely, if you have been granted 1000 shares, and there are 10,000,000 shares total, you’ve been given .01%. If the company is sold for $10,000,000 total (and you’d vested all your shares), in the first example your shares would be worth $100,000. In the second… $1000.

That’s why you should always roll your eyes when you hear some idiot bragging about how many shares they got in their grant. Great, awesome that you got 20,000 shares. Do you know how many shares there are in total? Or what the strike price is? Because otherwise you know absolutely nothing.

Finding more information about your ISO grant

Now we know that we have to figure out the share price and total number of shares to understand the present and future value of the grant, it’s pretty clear that we’ll need to do some research. In some cases, you can just ask for those numbers, but companies can be secretive if they are raising funding or don’t want to disclose their valuation. Either way, we’ll assume for the purposes of this post that you need to find some of this information on your own.

It’s a little easier to run through this in a real life scenario. Take yourself back to March of 2011. Let’s pretend you applied to a tiny upstart ridesharing service called “Uber”, and they’ve decided you’ve got what it takes to help them take over the world. Your offer from Uber includes an ISO grant for 600,000 shares over 4 years. That sounds like a bundle, but as we learned before, it’s impossible to know without doing some further research.

Luckily, the interwebs make it easy to find ballpark figures for this stuff. For instance, CrunchBase has a relatively complete history of funding rounds for almost every startup (besides the really tiny ones). Looking at Uber’s funding, we can see that in February of 2011 they raised $11m in a Series A, with a $60m valuation.

This isn’t enough to find the value per share however, because we don’t know how many shares there are or the price per share. Because of, well, math, you need at least two things to figure out the third.

Total company value = $60,000,000= [$Price per Share] x [Number of Shares]

However, we can take a look at PitchBook data (caution: might need to finagle a trial for this) which shows that after that same round, each share was valued at $0.09. This allows us to arrive at both the total number of shares, and the current value of the grant.

Total shares: $60,000,000 (total valuation) / $0.09 (price per share) = 660,000,000 shares (+-)

Grant value: $0.09 (price per share) x 600,000 shares = $54,000 (this is how much you pay to exercise your shares)

Now that we know the total number of shares, we can also see the total percentage our 60,000 share grant is equal to: 600,000 / 660,000,000 = .0009, or .09%. That’s almost a tenth of a percent of the company, which sounds ridiculously small… except when you realize that Uber is worth more than $50b, according to their last valuation in 2017. That’s $45,000,000, at current value, for stock that you would only have to pay $54,000.

Caveats, caveats everywhere!

That number sounds pretty awesome, doesn’t it? Time to pull up the air stairs on the Gulfstream and jet down to Mexico and… no. Here are the caveats to everything I just described:

This is not a likely scenario in the first place: Although there likely ARE some lucky bastards who got a similar deal or better at Uber in their early days, most of us will never see an opportunity like that in our lifetimes. Most companies fail, leaving you with absolutely nothing. If they don’t fail, only a rare and small percentage are ever worth more than $1b, let alone $50b. Seriously, pay attention to this caveat… most options expire worthless.

Shares get diluted: Uber has had about 10 funding rounds since 2011, each one of which created more shares, causing your shares to be diluted. In plain English, there are more shares in the total pool but you didn’t get any more, so you own less of the total. More than likely, another 500m-1b shares have been created, causing your .09% equity stake to fall to .04% or worse.

Most people join companies later than the first round: To get a deal like the one I described above, you have to join a company when it’s 10-20 people… MAX. That doesn’t leave very many opportunities. Now, even if you joined Uber in 2013 or 2014, things would still be looking good, but you would’ve received fewer shares at a much, much, much higher strike price.

People leave companies: What if you decide to leave after two years to work at Lyft? Then you’ll only see half of your shares, and that’s only if you purchase them. That means you have to come up with $27,000 (half of the total exercise cost of $54,000, because you stayed for half of your vesting period). Even then…

You have to be able to SELL your shares to profit from them: Uber isn’t publicly traded. Although there are private markets, it’s a pain in the ass to get rid of your shares, and you’ll have to take a steep discount.

Uncle Sam... At a minimum, you will pay 15% of every dollar you earn from your options. For various reasons that will be discussed later, often people end up paying taxes on their ISO gains as income, which can be well over 30%. Don’t get hung up on the details here, it’s seriously confusing and involves a relic called the AMT; the point is you should expect to pay some major taxes.

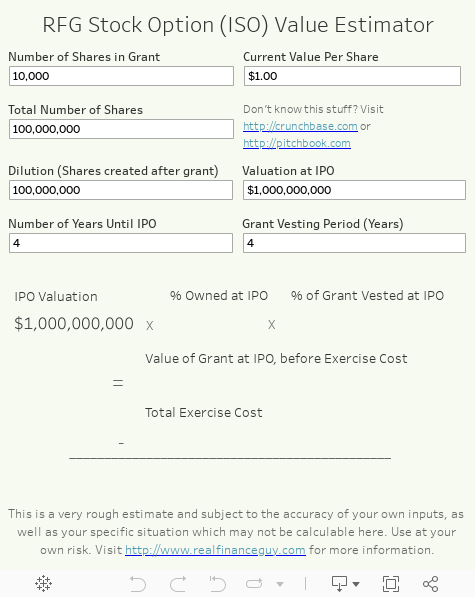

How much are my stock options worth?

The Tableau Public visualization below will allow you to ascertain the potential future value of your ISO stock grant, provided that the numbers you input actually make sense. Trust me, I am the king of optimistic numbers… be a pessimist when you enter this stuff and you will be pleasantly surprised. The value of stock options is determined by a couple of things:

The number of shares in your grant

The current value of your shares (per share)

The total number of shares outstanding (“Fully diluted shares”)

The vesting period for your shares (how many years will it take to vest)

A GUESS for how much your company will be worth at IPO or acquisition

A GUESS for how many new shares will be created before IPO (dilution from further fundraising and option grants… make sure to put a big number in here to be conservative)

A GUESS for how many years it’ll be until your company IPOs or is acquired

Note that because there are three GUESSES above, the accuracy of this calculator is determined by the accuracy of the numbers you put in. Garbage in, garbage out!

ISO Grant Value Calculator

The back of the hand calculation

In case you don't have time for all of that noise, it's not too hard to wing a calculation, although it'll be much less accurate. You'll need the current valuation, along with the value of your grant. Then, guess how much the company will IPO for. Now, do this math:

[Value of your grant]/[Current valuation]= [Percentage ownership]

([Percentage Ownership]x[Value at IPO])-[Value of your Grant]=[Take home])

Subject to taxes of course.